Why you need a deposit bond in your professional toolkit?

Our Blog

Guest Post: by Jared Zak from Dott & Crossitt Deposit bonds are being used increasingly in New South Wales and Queensland conveyancing transactions as an alternative to cash deposits. A deposit bond is essentially a promise given by a highly-rated financial institution to pay a vendor a sum equal to ten percent (or occasionally five percent)… Read more »

As we’ve seen recently, when developers and builders go into liquidation, the danger for your customers is that their cash deposit could potentially be tied up for years as the liquidation plays out. Even worse, their cash deposit could disappear – check out this recent news article here So in the current market when you are acting… Read more »

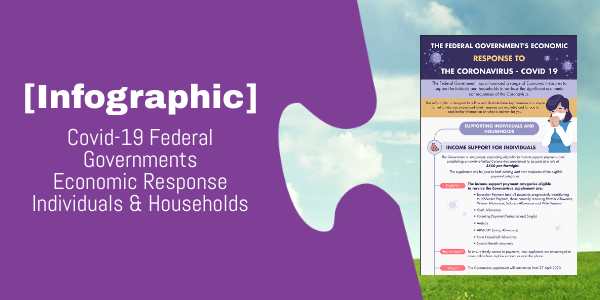

This infographic is designed to collate and illustrate the key measures the Federal Government has taken in response to The Coronavirus – COVID 19.

Ever wondered where deposit bonds came from? Deposit bonds, also known as deposit guarantees, have been helping Australians buy houses for almost two decades. So how did it all begin?

What supporting documents do you need to get a deposit bond? Why do you need them? And how do you supply them? Find out everything you need to know about supporting documents in this guide.

Got the cash for the deposit but can’t get to it in time? We’ve got the lowdown on 3 potential solutions.

![]()

Lets work together

Get access and the ability to

Lodge & Manage Deposit Bonds for your clients

Lodge & Manage Deposit Bonds for your clients- Access to your own personalised portal

- Generate commissions for every Deposit Bond lodged

Apply for a deposit bond

- Purchasing as an individual.

- Settling within 6 months.

- Proof of funds to complete purchase: either finance approval or other proof of funds like a sale contract.

![]()

Concierge Service

We will make the process so simple for you by applying for your deposit bond for you! Use our concierge service for your deposit bond application

See real-life stories

Seeing other people’s dreams come true is pretty magical. Especially when it could be you.

Blog – Get expert

advice and tips

Are you a first homebuyer wondering how a deposit bond can help you? Not sure what to do next? Read on..

Read More